Market to World: The War is Over?

© 2026 Sarmaya Partners, LLC

May 4, 2026

While complacently ignoring the impending aftershocks

Bottom Line Upfront:

- The escalation vs. de-escalation back-and-forth has already resumed. Iran re-closed the Strait over the weekend of April 18-19, and we expect this volatility to continue.

- However, as far as the market is concerned, based on price action, the war is over. Looking at past geopolitical crises has worked in the past for the market as things normalize soon after the event.

We believe this approach ignores the aftershocks of this geopolitical earthquake that economies, companies and consumers are only now beginning to feel and will last for months and quarters to come. While there is the possibility consensus may prove correct, we view that as the less likely outcome given the enormity of the oil supply shock.

While complacently ignoring the impending aftershocks

Bottom Line Upfront:

- The escalation vs. de-escalation back-and-forth has already resumed. Iran re-closed the Strait over the weekend of April 18-19, and we expect this volatility to continue.

- However, as far as the market is concerned, based on price action, the war is over. Looking at past geopolitical crises has worked in the past for the market as things normalize soon after the event.

We believe this approach ignores the aftershocks of this geopolitical earthquake that economies, companies and consumers are only now beginning to feel and will last for months and quarters to come. While there is the possibility consensus may prove correct, we view that as the less likely outcome given the enormity of the oil supply shock.

War is Over?

History shows that the markets begin pricing in events that are likely to occur even before they’re finalized. In the case of geopolitical events investors have historically been rewarded for looking past these crises, which typically have not left lasting negative impacts. Taking a page out of that playbook, since the initial ceasefire announcement the market has been treating the war as winding down and moved into a negotiations phase.

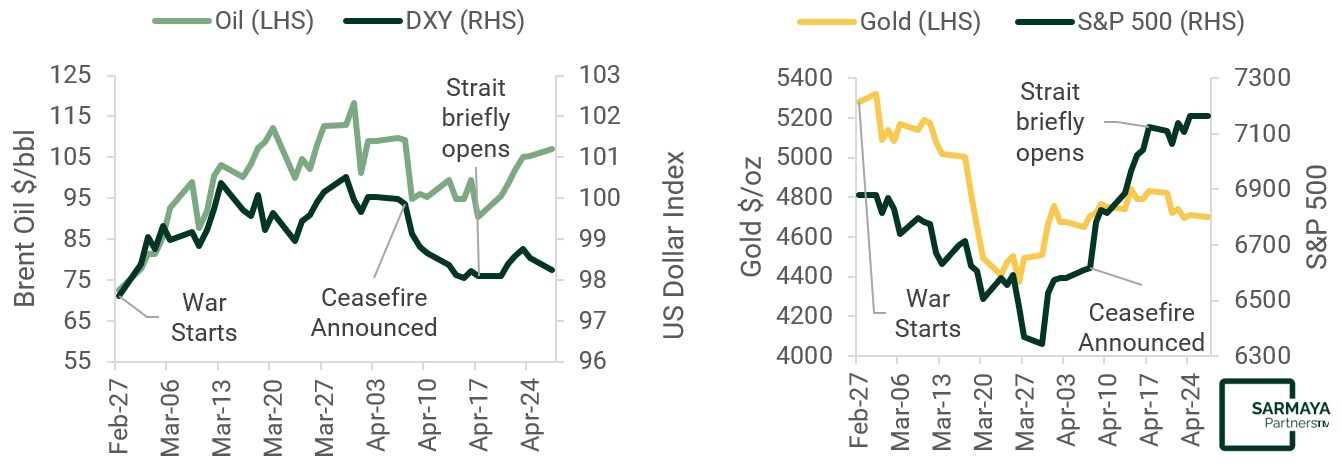

The announcement of the ceasefire during the week of April 5 was the beginning of this new phase and the price action of some assets began to reflect that. Despite the escalation headlines of “war on, war off” creating volatility, asset prices have moved in the “war is over” direction. Oil and the U.S. dollar have weakened, while gold has climbed higher, and equities rallied on relief. To be fair, part of the equity rally likely reflects anticipation of strong Q1 2026 earnings, not just relief on the ceasefire. But earnings are a rear-view mirror. Whatever Q1 2026 looked like, the economic damage from the Strait’s closure is a forward problem that hasn’t yet hit the numbers.

Markets are pricing de-escalation

Source: Sarmaya Partners, Bloomberg

As of 4/24/2026

That optimism didn’t survive the weekend. Within 48 hours of the Strait reopening, Iran reversed course – reasserting control over the waterway after the U.S. Navy fired on and seized an Iranian-flagged vessel. Oil retraced much of Friday’s losses. As noted before, the ‘war on, war off’ back-and-forth that we expected has already begun – while the risks of the impending energy supply shocks haven’t changed regardless of which headline wins the next news cycle.

The market is only focused on the immediate future and is complacently reflecting the investor consensus of “nothing ever happens to it.” But this war’s actual end, whenever it does happen, isn’t the end of its consequences. That’s because one of this conflict’s unique weapons is geography – specifically, the Strait of Hormuz. The Strait’s closure was like an explosion whose shockwaves have yet to be felt. The energy shock and consequences emanating from this closure will last for many months.

Now What? The Long Restart

The equity market move reflects investor complacency and myopia that is blind to the lagged effects of this energy supply shock. Even when wars end, their economic consequences take much longer to work through the system.

We believe there simply isn’t enough oil and gas to meet current global demand. Consequently, we’ll likely see a combination of rising prices and declining demand to bring the physical energy market to balance.

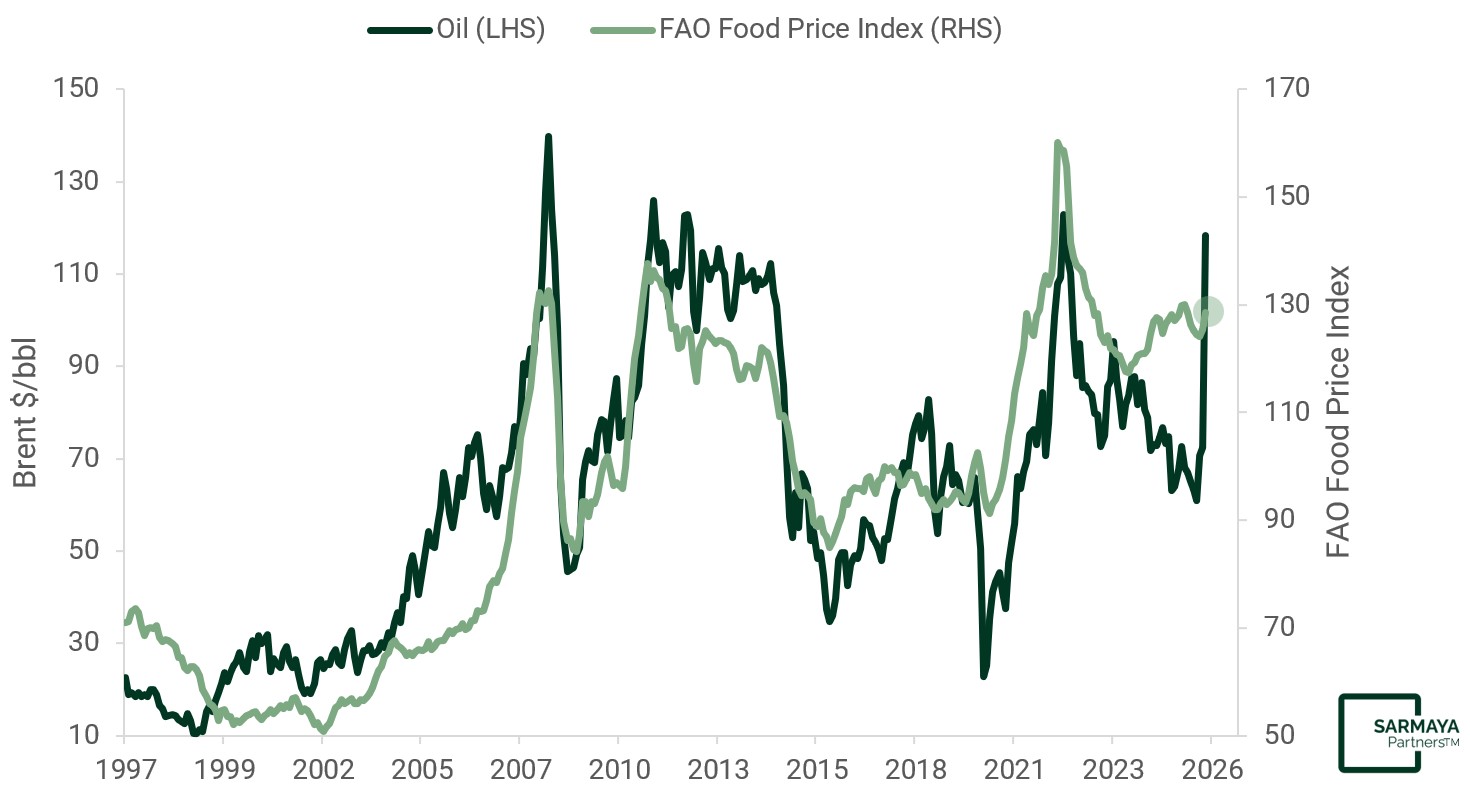

We expect restarting the energy supply chain to would likely take months. Layered on top are the lagged effects – fertilizer shortages pushing food prices up, rising packaging costs feeding into goods prices – all of which will keep inflation elevated. Rebuilding disrupted production, repairing infrastructure, renegotiating contracts, and restoring logistical capacity take time, often measured in quarters, not weeks. Energy is the input cost that touches everything. When it is disrupted at scale, inflationary echoes have historically persisted long after the initial shock.

Oil spikes often precede food inflation

Source: Sarmaya Partners, Bloomberg

As of 3/31/2026

The risk is that the economy slows more than currently anticipated. Markets are trading the ceasefire headline and ignoring the potentially looming economic hangover.

Looking Further Out: Return to Tangibles to Accelerate

There is a risk that an energy-driven consumer slowdown coincides with a slowdown in AI spending, even as credit concerns persist – leading to two of the primary engines of the current expansion losing steam at once.

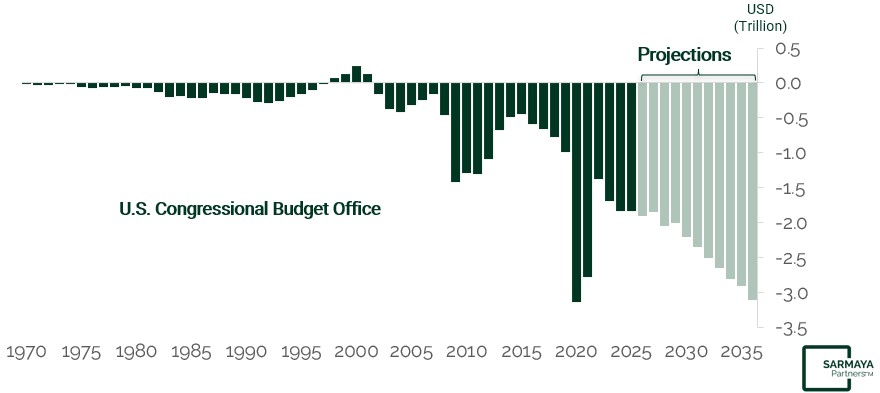

As a result, financial conditions might be weak enough for the Fed to pivot and provide support and stimulus. To be fair, not all the Fed’s prior pivots have resulted in inflation. We believe this potential pivot could be the accelerant that adds fuel to the inflation and debasement fire in this era of fiscal dominance.

Fiscal trends unsustainable

Source: Sarmaya Partners, Congressional Budget Office; Office of Management and Budget

Projections per CBO February 2026 Baseline. As of 2/11/2026

Consequently, we believe that this time, the primary beneficiaries of a Fed pivot will be tangible assets. This is the setup we have been describing for some time. The Return to Tangibles is not a single-event trade. It is a secular theme, and the aftershocks of this war may well provide the next catalyst. The structural forces we identified – higher for longer inflation, elevated geopolitical and fiscal risks, and the world continuing to build the future – are still unfolding. The pendulum has further to swing, although it has the potential to be interrupted or invalidated by changes in inflation, demand, policy, technology, or investor risk appetite.

Note: These thematic views do not constitute a recommendation to buy or sell any security or commodity. Commodity investments involve risks including price volatility, geopolitical disruption, and regulatory change.

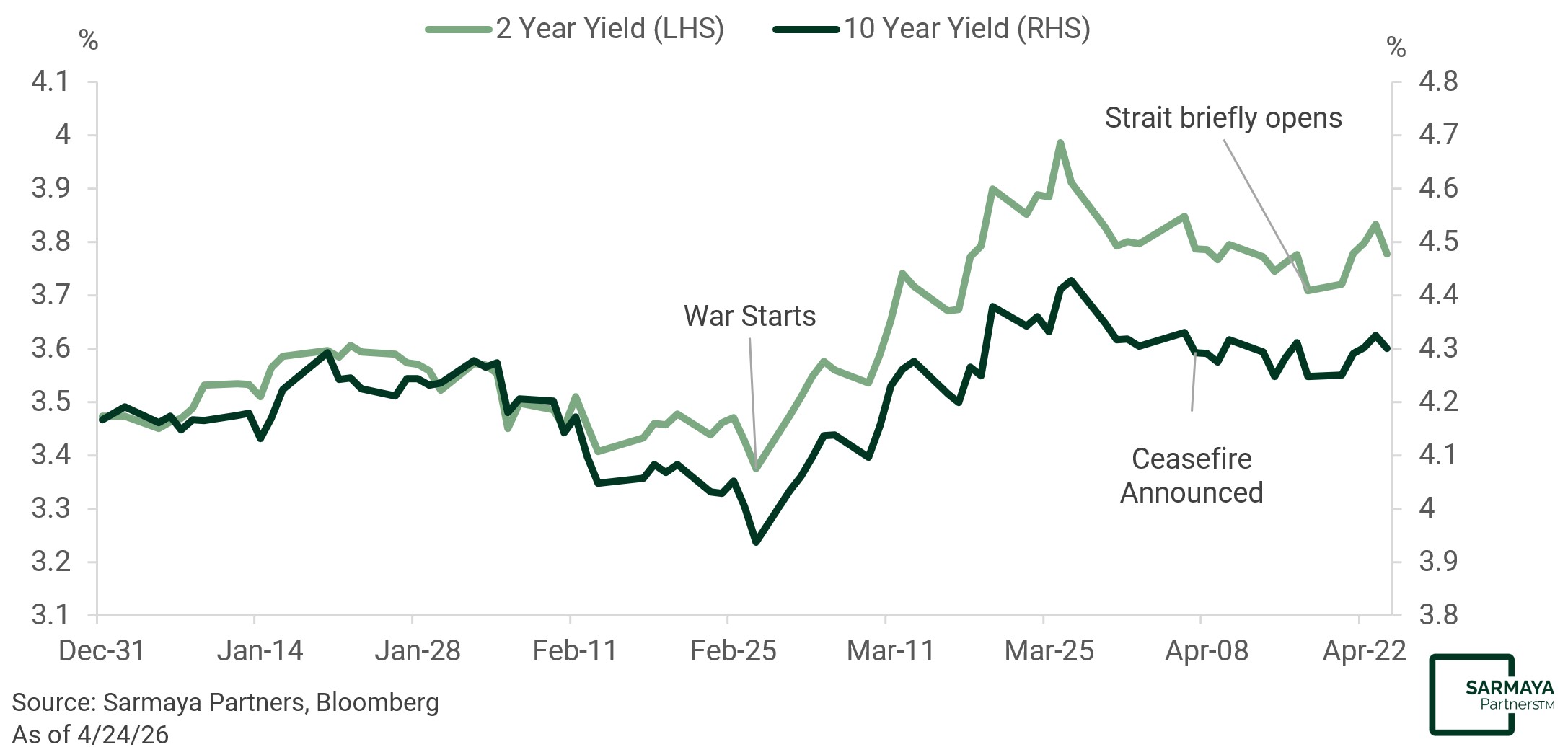

War triggered pain in rates

Source: Sarmaya Partners, Bloomberg

As of 4/24/26

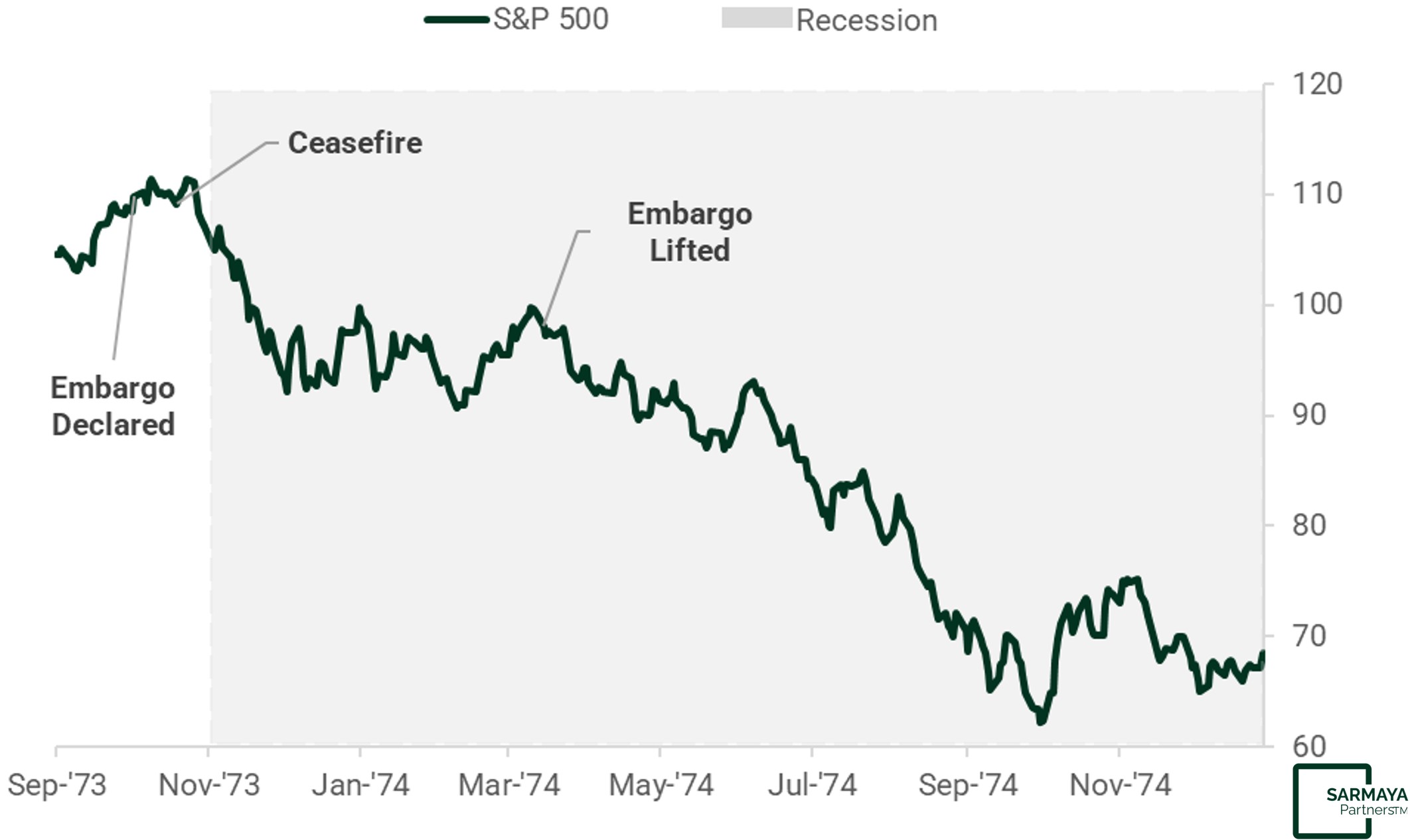

The 1973-74 analog is informative. From the embargo’s declaration in October 1973 to the market’s trough in late 1974, the S&P fell roughly 45%. Notably, the market rallied into the ceasefire… and then rolled over.

Importantly, the bulk of the drawdown came after the fighting ended, as the economic hangover from the energy shock worked its way through inflation, demand, and earnings.

Market did worse after oil embargo was lifted

Source: Sarmaya Partners, Bloomberg

As of 12/31/1974

Note: The 1973-74 period is presented for illustrative purpose only. Historical market analogs are not predictive of future results, and current market conditions, policy environments, and economic structures differ materially from those of the prior period.

Disclosures

Sarmaya Partners, LLC is a registered investment adviser with the U.S. Securities and Exchange Commission. SEC registration does not imply a certain level of skill or training.

This material is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security, strategy, or investment product. Nothing herein should be construed as investment, legal, tax, or accounting advice.

The views expressed reflect Sarmaya Partners’ opinions as of the date of publication and are subject to change without notice. These views represent the firm’s current assessment of market conditions and do not account for any individual investor’s financial situation, objectives, or risk tolerance.

This material contains forward-looking statements based on the firm’s current expectations regarding inflation, energy markets, monetary policy, and asset class performance. Forward-looking statements are inherently uncertain and actual outcomes may differ materially. Readers should not place undue reliance on such statements.

References to the 1973–74 oil embargo are for illustrative purposes only. Historical events are not predictive of future results. Current market conditions, policy environments, and geopolitical dynamics differ materially from past episodes, and similar outcomes should not be assumed.

References to specific asset classes, commodities, or investment themes, including the “Return to Tangibles” framework, reflect the firm’s current market outlook and do not constitute a recommendation to buy or sell any security or commodity. Commodity and natural resource investments involve risks including price volatility, geopolitical disruption, supply and demand uncertainty, and regulatory change. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal.

Certain data has been obtained from third-party sources including Bloomberg and the Congressional Budget Office. While believed to be reliable, Sarmaya Partners makes no representation as to its accuracy or completeness.

© 2026 Sarmaya Partners, LLC. This material may not be reproduced or distributed without prior written consent.

May 4, 2026